CONTACT OUR TEAM TODAY

admin@withersco.co.nz

(09) 425 8599

As we step into a new financial year, we’re mindful that not everyone has had a smooth start to 2026. Extreme weather has created uncertainty for parts of the country and reminded many businesses just how quickly conditions can change. The global situation has intensified that.

While we can’t control everything that happens around us, we can make sure we’re prepared for shifts when they come.

That starts with a clear understanding of your finances, staying on top of compliance, and planning ahead rather than reacting under pressure.

In this issue, we cover three key employment and tax changes you need to know (and two to keep an eye on), how to get more value from your accountant, and the signs that business confidence in New Zealand is steadily improving.

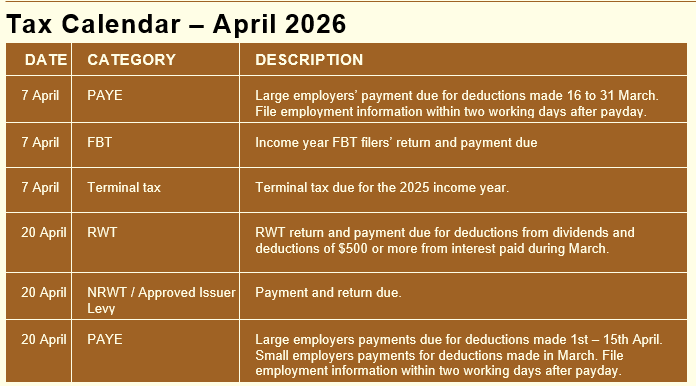

Three key changes for employers in 2026

A few recent and upcoming changes may impact your payroll, pricing, and employer obligations. A quick check now sets you up for a smoother year ahead.

1. Minimum wage is increasing

From 1 April 2026, the adult minimum wage rises to $23.95/hr (from $23.50). Starting-out and training wages increase to $19.16/hr (from $18.80).

Make sure your payroll and employment agreements reflect the new rates. Higher wages can affect your margins, so now’s a good time to reassess your pricing structure. Speak to your accountant if you need help understanding what these changes mean for your bottom line.

2. KiwiSaver contribution rates go up

Also starting 1 April 2026, the default KiwiSaver contribution rate increases from 3% to 3.5% for both employees and employers. Note employees are able to apply for temporary rate reductions to continue contributing at the 3% rate, in which case employers may also opt to match this employer contribution rate. Employer contributions will also now apply to KiwiSaver members aged 16 and 17. This is part of a phased retirement-savings policy change, with a further rise to 4% planned for 2028.

Review your payroll processes to make sure your contributions are applied correctly.

3. Fringe Benefit Tax updates continue

Updated FBT thresholds and rate structures came into effect on 1 April 2025, with further refinements expected to be rolled out in 2026. Concessions such as equalisation of FBT and PAYE on unclassified benefits give you more flexibility in how FBT is calculated and means the tax rate applied better reflects what your employees earn.

Inland Revenue has also clarified how certain employee gift cards are taxed. Open-loop cards (such as prepaid cards that can be used almost anywhere) are generally treated like cash and taxed under PAYE, while retailer-specific cards usually still fall under FBT. If you provide vouchers or gift cards as staff rewards, it’s worth checking they’re being taxed under the right rules.

Things to watch

Keep an eye out for these two changes on the horizon.

Shareholder loans

If you regularly draw funds from your company through a shareholder loan, this is one to watch. While not yet law, Inland Revenue has recently consulted on proposals to treat new shareholder loans as taxable dividends if they are not repaid within a set timeframe.

Surcharge ban

The Retail Payment System Amendment Bill has passed its first reading and is expected to take effect by May 2026. If enacted, it will ban most in-store surcharges on EFTPOS, Visa, and Mastercard transactions.

We’ll keep you updated as details are finalised.

Is it time to look at your business with fresh eyes?

Tax returns and year-end accounts are essential, but the real value lies in treating your accountant as an advisor: someone who helps shape where your business is heading, not just where it’s been.

A proactive conversation early in the year can help you:

• Plan for tax rather than react to it

Provisional tax shouldn’t come as a surprise. We can model expected profit, test different scenarios, and give you a clear estimate of what you’re likely to owe well before payment dates hit.

• Understand your break-even point and profit margins

Do you know exactly how much revenue you need each month to cover fixed costs? We can calculate your break-even point and identify which products or services are truly driving profit (and which may be quietly eroding it).

• Forecast cashflow and stress-test growth plans

Mapping your cash inflows and outflows each month gives you clarity when you ask questions like: What happens if sales slow for a quarter? If a key client pays late? If costs creep up again? It’s far easier to make small course corrections early than face a cash squeeze later.

• Check whether pricing still reflects your cost base

Between minimum wage increases and supplier cost rises, margins can tighten without you noticing. A quick pricing review can protect profitability before pressure builds.

• Think about how you pay yourself

Your business income and personal finances are closely connected. Being deliberate about how you take money out of the business can help prevent tax surprises and keep cashflow steady throughout the year.

• Strengthen conversations with your bank or lenders

Clear forecasts and well-prepared financial summaries from your accountant demonstrate viability and repayment capacity. That preparation often changes the tone of lending conversations entirely.

If you’d like 2026 to feel more strategic than stressful, now is a good time to schedule a conversation.

CONTACT OUR TEAM TODAY

admin@withersco.co.nz

(09) 425 8599

21 Neville Street

PO Box 113

Warkworth 0910, New Zealand